AFRICA’S ENERGY SYSTEM TODAY: STATUS, CHALLENGES AND OPPORTUNITIES

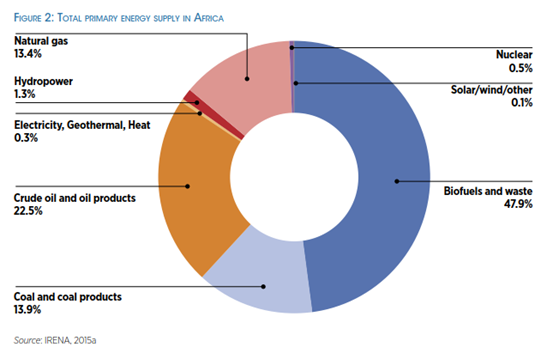

The total primary energy supply (TPES) in Africa has more than tripled since 1971 and has been growing at around 3% per year, one of the most rapid rates for any region (IRENA, 2015a). Despite this growth, Africa is still highly dependent on traditional biomass (Figure 2), and modern energy use on the continent remains low, with no other region of the world having such a high share of traditional biomass use in TPES. In some African countries there is very little modern energy service provision: for example, the share of bioenergy is more than 90% in Burundi, the Central African Republic and Rwanda (IRENA, 2013a).

In 2013, oil accounted for about 22% of Africa’s TPES, but the continent exports more than 80% of the oil it produces. Hydropower, wind, solar and nuclear account for 2-3% of the TPES. TPES per capita on the continent is among the lowest in the world, at around 0.7 tonnes of energy equivalent (toe) per capita (0.6 toe/capita in sub-Saharan Africa) (IEA, 2014a). It is around one-sixth of the TPES per capita in OECD countries, at over 4 toe/capita. Excluding traditional biomass use would raise this ratio significantly.

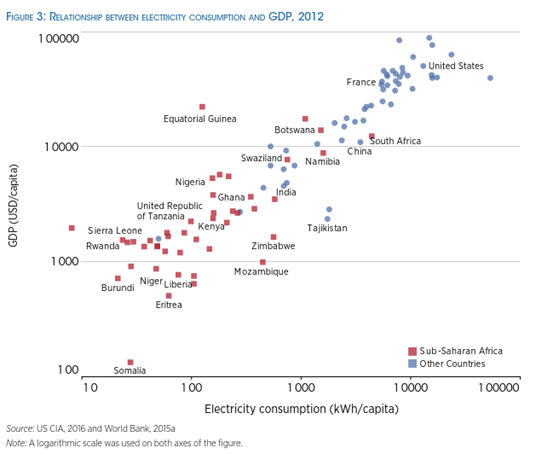

Access to adequate energy supplies and economic growth are interlinked. It therefore is no surprise to see that electricity consumption per capita in Africa is low (Figure 3). Yet even on this relative benchmark, some African countries perform poorly. Electricity consumption per capita is significantly lower in some sub-Saharan African countries even compared to other countries with similar levels of per capita gross domestic product (GDP) (e.g., Tanzania compared to Tajikistan). Electricity production per capita in 2012 in Africa averaged 664 kilowatt-hours (kWh), compared to 9 170 kWh per capita in the OECD countries and the global average of 3 220 kWh per capita.

When compared to OECD countries, the difference is stark. For example, Nigeria’s and Kenya’s electricity consumption per capita are 147 kWh and 153 kWh, respectively, compared to 12 210 kWh in the United States and 6 869 kWh in France. Electricity consumption per capita in these two OECD countries is 45 to 83 times higher than in Nigeria and Kenya (Africa Progress Panel, 2015).

This reflects a range of factors, but two factors largely drive this dynamic:

Low electricity access rates in sub-Saharan Africa.

Investment in electricity generating assets that has lagged behind underlying demand growth.

This has led to low rates of electricity consumption, even compared to income levels in some countries, and insufficient investment in generation capacity has had severe economic consequences. Addressing the deficiency in electricity generating capacity and, critically, output, given the significant unavailability of existing thermal and often hydropower plants, as well as improving electrification rates, would reap huge social and economic dividends. The energy sector bottlenecks and power shortages cost the region 2-4% of GDP annually, undermining sustainable economic growth, jobs and investment (Africa Progress Panel, 2015). The costs are not just economic, but also social. Africa’s poorest people are paying among the world’s highest prices for energy services: householders in a village in northern Nigeria spend around 60 to 80 times more for each unit of useful light than a resident of New York City or London.

Electricity access

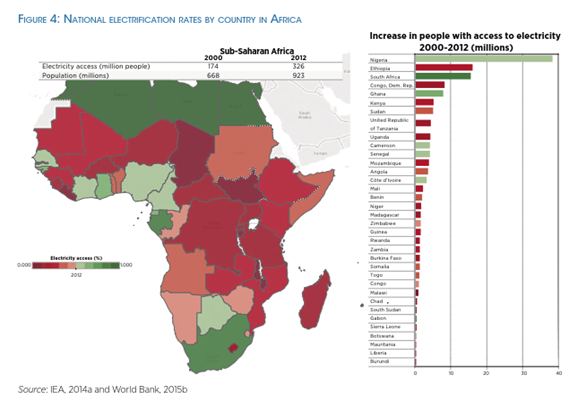

The electrification rate (the percentage of the population with access to electricity) in sub-Saharan Africa is the lowest of any developing region. Electrification rates in sub-Saharan Africa rose from 22.7% in 1990 to 26.1% in 2000, and reached 35% in 2012 (World Bank, 2015a). Every country in sub-Saharan Africa has seen electrification rates rise between 2000 and 2012, except The Gambia, where the percentage rate was roughly constant (Figure 4). With population growth between 2000 and 2012, this has resulted in 150 million sub-Saharan Africans gaining access to electricity since the year 2000.

The situation is not aided by the high incidence of poverty in Africa and by the challenges that many Africans face in paying for modern energy services. Africans with irregular and extremely low incomes struggle to pay for modern energy services, and they end up paying relatively high prices for poor-quality energy services (e.g., the use of candles or kerosene lanterns). However, in recent years a growing African middle class13 and access to low-cost lighting imports have caused rapid shifts in the lighting share in some countries, as Africans shifted from kerosene to LED lights powered by batteries, solar lanterns or SHS kits.

Significantly improving the electrification picture is not just a challenge, but a huge investment opportunity that increasingly is being met by socially conscious entrepreneurs. Millions of energy-poor, disconnected Africans, who earn less than USD 2.50 a day, already constitute a USD 10 billion yearly energy market (Africa Progress Panel, 2015). Despite the small-scale nature of individual transactions and a range of other difficulties, the opportunities for providing clean, sustainable renewable power rapidly to Africa’s rural communities via SHS and solar PV mini-grids represents an exciting development opportunity.

Energy service quality

Underpinning the relatively modest track record for electricity access and investment in supply is a lack of adequate infrastructure in Africa. This also is true for the electricity network. Around two-thirds of the countries in sub-Saharan Africa have transmission networks where 50% or more of the lines are at least 30 years old (EC JRC, 2014). Even in South Africa, 30% of transmission lines are at least 30 years old. The chronic lack of investment in infrastructure, leading to challenges with maintenance and aged infrastructure, all contribute to the very common blackouts of grid power supply in sub-Saharan Africa.

As a result, and due to inadequate supply capacity, even where modern energy services are available, quality can be lacking. Electricity supply in sub-Saharan Africa is often unreliable, with blackouts and brownouts the norm in many countries, and unmet demand means that economic growth is lower than it otherwise might be. The inability of power generation capability to grow to meet the underlying demand for electricity in Africa is creating one of the continent’s greatest challenges. The costs are felt across the African economy and, in some countries, are crippling. African manufacturing enterprises experience on average 56 days per year of power outages. Companies lose 6% of sales revenues in the manufacturing sector, and the losses can go as high as 20% when back- up generation is not available and/or expensive

(World Bank, 2015b).

The reasons for the crises in many African electricity systems are varied and differ by country. However, common causes are: drought (affecting hydropower capacity), poor maintenance (often related to poor utility revenues and profitability) that reduces plant availability, systems disrupted by conflict (it can take years or decades after a conflict ends for the electricity sector to recover), and high demand growth and structural issues in the electricity sector that have held back investment in supply, transmission and distribution (World Bank, 2008). Another challenge is the generally difficult business environment that exists in Africa.

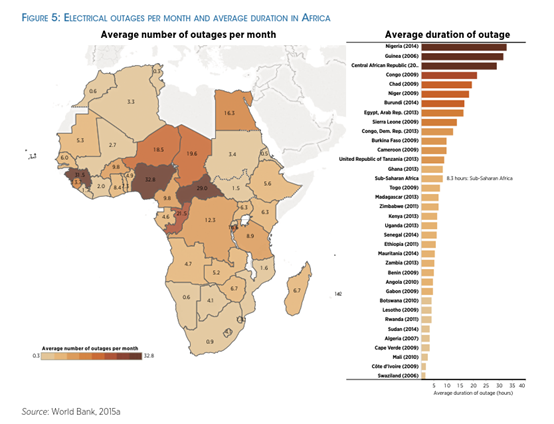

Figure 5 highlights just how serious the underinvestment in power generation capacity is in sub-Saharan Africa. Eleven countries in Africa experience an average of 10 or more electrical outages per month, and five experience an average of 20 outages or more per month (World Bank, 2015c). The average duration of these outages in sub-Saharan Africa was 4.6 hours, with 17 countries having outage durations that exceed this average.

Yet the situation is not static, as the demand for electricity is expected to grow rapidly in Africa in coming decades. By 2100, Africa’s population could quadruple, making it home to more than 4.4 billion people (UNDP, 2015). Most of the growth will occur in the sub-Saharan region. With growing economies and rising standards of living in Africa, in the next 15 years alone electricity demand is expected to grow more than three-fold (IRENA, 2015a). This continued rapid growth will require large investments just to ensure that electricity supply quality does not deteriorate and that electricity access levels do not decline due to population growth outstripping new connections.